5 Crypto Banking Myths That Keep You Broke

Crypto banking, which includes services like cryptocurrency custody, decentralized finance (DeFi) platforms, and virtual asset service providers (VASPs), has grown significantly in recent years. However, persistent myths continue to deter potential users, potentially limiting financial opportunities. This analysis, based on credible information as of October 23, 2025, examines and debunks five key myths: lack of regulation, excessive risk, fake yields, inability to spend crypto, and exclusivity to tech-savvy individuals. The objective is to provide a balanced, evidence-based overview, highlighting both advancements and ongoing challenges in the crypto banking sector.

Myth 1: Crypto Banking Isn't Regulated

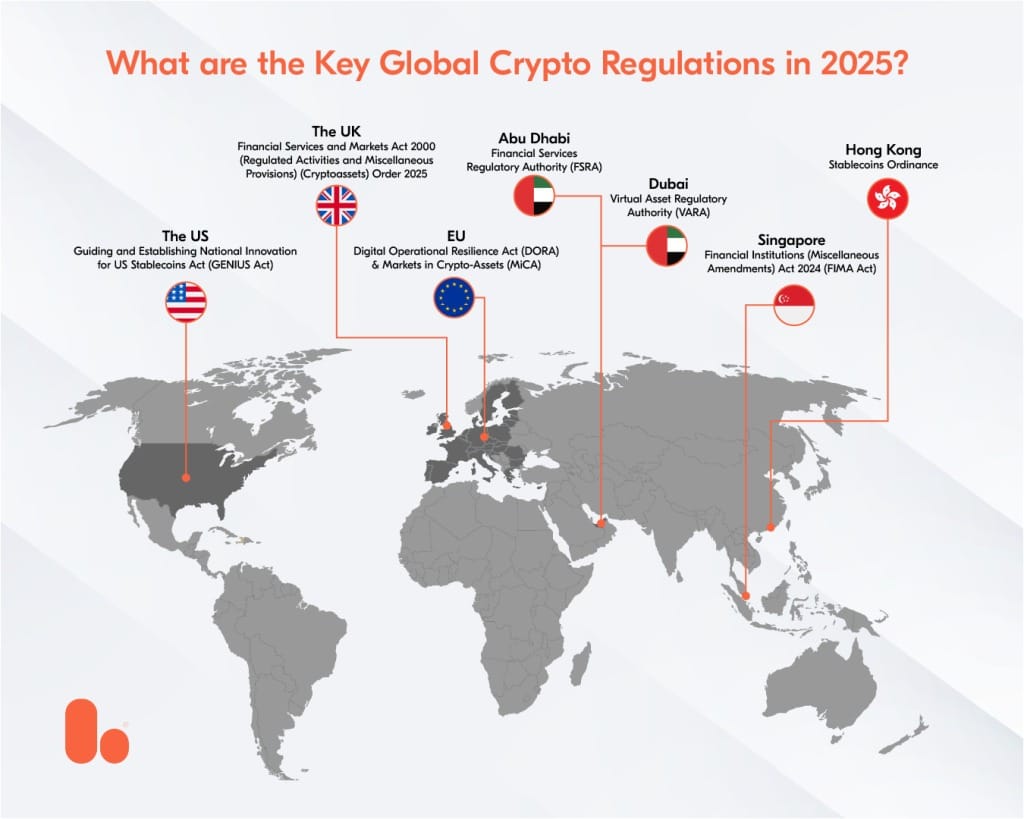

One of the most widespread misconceptions is that crypto banking operates without oversight, resembling an unregulated frontier. In reality, VASPs (entities that facilitate crypto exchanges, custody, or transfers) are subject to robust regulatory frameworks globally.

Key regulations include guidelines emphasizing anti-money laundering (AML) and counter-terrorist financing (CTF) for virtual assets. In the European Union, regulations effective in 2024 require licensing for crypto platforms, focusing on consumer protection and transparency. The United States employs a combination of federal laws and state-specific regulations, such as New York's BitLicense requirements, mandating Know Your Customer (KYC) compliance and regular audits.

Rules requiring VASPs to share transaction data mirror traditional banking's compliance standards. While regulatory gaps exist (such as non-custodial wallets evading some oversight) the overall trend shows regulation is tightening, demonstrating that crypto banking is increasingly aligned with traditional finance oversight mechanisms.

Myth 2: It's Too Risky

Critics often characterize crypto banking as inherently dangerous due to market volatility and past security breaches. However, institutional-grade custody solutions have evolved substantially to mitigate these risks, making them comparable to traditional banking safeguards.

Banking regulators have issued comprehensive guidance on crypto-asset safekeeping, emphasizing tailored risk management for cryptographic keys. Financial institutions now offer custody solutions featuring multi-signature security protocols, insurance coverage, and cold storage systems, significantly reducing exposure to hacking incidents. A 2025 statement from federal agencies confirms that standard custodial principles apply to crypto assets, with necessary adaptations for their unique risk characteristics.

Industry audits emphasize rigorous controls for key management, acknowledging that while price volatility persists, operational risks can be effectively managed. Regulators have clarified banks' authority for crypto-related activities, requiring strong risk controls comparable to traditional financial services. Despite past incidents like the 2022 FTX collapse, the sector's maturation (with billions in secured assets) demonstrates that risk is manageable through proper due diligence, rather than being inherently prohibitive.

Myth 3: Yields Are Fake

Skeptics frequently dismiss crypto yields (sometimes ranging from 5-20% APY in DeFi) as Ponzi schemes. However, DeFi yields have a legitimate economic foundation. Unlike traditional banks that profit by lending depositor funds at a spread, DeFi platforms generate yields through protocol fees, liquidity provision, and staking rewards.

"Real yield" in DeFi refers to returns derived from protocol revenues, such as trading fees, loan interest, or staking rewards, rather than inflationary token emissions. For example, staking on proof-of-stake blockchains generates yields from network transaction fees. Yield farming involves providing liquidity or lending tokens through smart contracts, earning returns from borrower interest or transaction fees paid by platform users.

While fraudulent schemes exist (such as rug pulls in unvetted projects) DeFi's inherent transparency allows users to verify economic models through independent audits and on-chain data analysis. Critics correctly note that some protocols lack substantive real-world utility, but established platforms derive yields from genuine economic activity. In 2025, the industry focus on sustainable yields confirms that not all returns are fabricated, though investors must remain aware of volatility and impermanent loss risks.

Myth 4: You Can't Spend Crypto

A common misconception is that cryptocurrencies are impractical for everyday spending, limited to speculative digital holdings. In practice, tools like crypto debit cards and ATMs enable seamless conversion to fiat currency.

Crypto debit cards allow users to spend Bitcoin, Ethereum, or stablecoins like USDC at millions of merchants worldwide, with instant conversion to local currency at the point of sale. ATMs supporting crypto transactions are expanding rapidly, with tens of thousands of units deployed globally as of 2025. These kiosks facilitate buying or selling crypto with cash or debit cards, effectively bypassing traditional banking infrastructure.

However, crypto ATMs have attracted regulatory scrutiny due to fraud concerns, with significant financial losses reported in 2025 from scammers exploiting these platforms. Some jurisdictions have enacted legislation limiting transaction amounts and mandating refund protections to address these issues. Despite these challenges, spending cryptocurrency is increasingly viable and expanding, particularly for cross-border payments utilizing stablecoins.

Myth 5: It's Only for Tech People

Many individuals assume crypto banking requires advanced technical knowledge, which alienates non-expert users. Recent user experience (UX) improvements have democratized access, making crypto banking significantly more user-friendly.

Fintech and blockchain platforms now prioritize intuitive design principles, with applications resembling conventional mobile banking interfaces for buying, staking, or trading digital assets. Industry best practices emphasize simplified interfaces that reduce barriers for all users regardless of technical skill level. Neobanks and DeFi platforms increasingly focus on addressing user needs rather than showcasing blockchain complexity.

For traditional banks entering the crypto space, success depends on seamless user experience rather than highlighting blockchain technical intricacies. Open banking integrations are enhancing accessibility, fostering greater competition and innovation in the sector. While a learning curve remains, the 2025 emphasis on user experience ensures crypto banking is becoming progressively more inclusive and accessible to mainstream users.

Conclusion

This analysis reveals that while legitimate challenges such as fraud and market volatility persist, many common myths about crypto banking are largely outdated. These misconceptions fail to reflect the significant regulatory and technological progress achieved in recent years. As the industry continues to mature, understanding the factual landscape of crypto banking becomes essential for investors and users seeking to make informed financial decisions.