Why 2026 Marks the End of Fragmented Finance and the Beginning of an On-Chain World

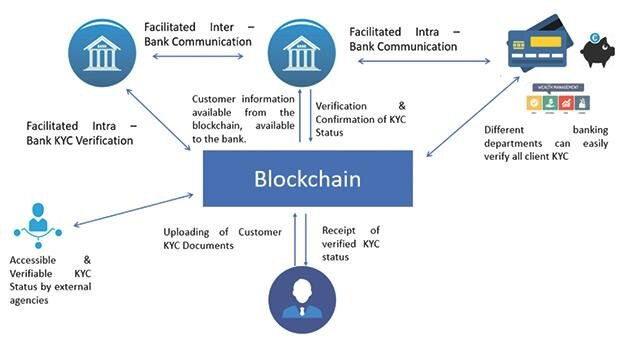

For decades, the global financial system has run on isolated islands of information. Banks, payment processors, regulators, and credit bureaus each maintain their own databases, their own customer IDs, their own versions of the truth. Moving money or proving identity across these borders has required intermediaries, manual reconciliations, and fees that often exceed the transaction itself.

That era is ending.

Blockchain’s shared, immutable ledger is systematically dismantling data silos. What began as an experiment in digital cash has become the default infrastructure for verifiable information. By the close of 2025, the shift is no longer theoretical; it is measurable in billions of dollars flowing across previously incompatible networks and in real-world institutions quietly migrating critical processes on-chain.

The Cost of the Old Model

Traditional financial data architecture is inherently duplicative. A single individual can exist as dozens of separate records across core banking systems, CRM platforms, anti-money-laundering tools, and compliance silos. Reconciliation errors, delayed settlements, and regulatory friction are not accidents; they are direct consequences of this fragmentation.

The numbers are sobering:

• Enterprises lose hundreds of billions annually to poor data integration and governance.

• Cross-border payments still take days and cost 6–7 % on average in hidden fees.

• Roughly 1.4 billion adults worldwide remain unbanked, largely because legacy systems cannot cost-effectively verify identity or credit history at scale.

These are not solvable problems within the existing paradigm. They are features of centralized, proprietary databases that were never designed to talk to one another.

The Rise of the Shared Ledger

Blockchain replaces private databases with a single, continuously reconciled source of truth. Every participant on the network maintains an identical copy of the ledger, updated in real time through cryptographic consensus. Once data is written, it cannot be altered retroactively without breaking the chain; an event visible to every observer.

The implications extend far beyond cryptocurrency:

• Supply-chain provenance becomes instantly verifiable (DHL and IBM Food Trust have already reduced fraud and disputes by double-digit percentages).

• Patient records can travel securely across providers without fax machines or middlemen.

• Humanitarian aid reaches recipients with full audit trails (UNICEF’s 2024–2025 blockchain programs delivered cash to 3.5 million households across 48 countries with near-perfect transparency).

Interoperability: The Tipping Point of 2024–2025

Isolated blockchains once replicated the silo problem at a new layer. That changed dramatically this year.

Cross-chain infrastructure matured into production-grade systems:

• Axelar processed more than $8.6 billion in volume across 64 networks.

• Total value locked in interoperability protocols surpassed $19 billion.

• Bridges and message-passing layers (LayerZero, Wormhole, IBC, Polkadot parachains) now move assets and data seamlessly between Ethereum, Solana, Cosmos hubs, and dozens of layer-2 ecosystems.

The result is a rapidly coalescing “internet of blockchains.” Assets, identity proofs, and credit histories are becoming portable in the same way web pages became portable after HTTP standardized in the 1990s.

Real-World Adoption Is Already Here

Institutions are no longer debating whether blockchain works; they are competing on who integrates it fastest.

• Ledn crossed $1 billion in outstanding Bitcoin-backed loans in 2025, proving on-chain collateral can scale with institutional-grade risk controls.

• Regulated platforms are bridging the gap between traditional finance and open networks. BxLend, one of the few fully EU-licensed Virtual Asset Service Providers focused on lending and spending, recently added Ian Scarffe (a European Commission advisor) to its team as it prepares for institutional inflows.

• On-chain lending markets (Aave, Compound, and newer compliant entrants) now offer yields that traditional savings accounts cannot match, backed by transparent, over-collateralized positions visible to anyone.

What This Means for Individuals

For the first time, everyday people can opt into a financial system that operates under different rules:

• Money and data move at internet speed with final settlement in minutes, not days.

• Yield is available on stable assets without relying on a bank’s discretionary interest rate.

• Ownership is provable and non-custodial; no third party can freeze or seize assets without on-chain justification.

Buying and holding crypto in late 2025 is no longer primarily a speculative bet on price appreciation. It is an active migration to infrastructure that is objectively superior to the fragmented, fee-heavy systems most of the world still uses by default.

The Window Is Closing Faster Than Most Realize

Every month brings another major silo breach, another legacy provider losing ground, another billion dollars flowing into open, verifiable networks. The off-ramps from the old system (regulated fiat on-ramps, user-friendly wallets, compliant lending platforms) are now abundant and improving weekly.

The data silos that defined finance for half a century are not evolving. They are collapsing under their own weight, replaced by a global, permissionless ledger that no single entity controls and everyone can audit.

The transition is already underway. The only question left is how early you choose to participate.